BY:

Informal remittance is still common in East Africa and is moving with the times

August 14th, 2023

Primary research conducted by FSD Kenya in conjunction with DMA Global in four remittance corridors in East Africa shows that the use of informal remittance channels is still common in the region giving key lessons for industry stakeholders.

Most conversations on remittances to (or in) Africa usually, at some point, lead to a discussion around what proportion, and what value, are sent through informal channels. Informal remittances are those sent through unlicenced or unregistered means. These flows have typically been cash-based; either in the form of cash physically carried across borders or sent with family and friends, cash given to bus drivers, or truck drivers that are crossing borders, or through unlicenced money transfer providers, including those using the hawala system.

By their very nature, informal remittances are undocumented and unrecorded and as such the scale and true value of them is unknown. Across Africa different numbers are banded around, with some analysts suggesting that informal remittances could account for as much as 50% of the total amount sent through formal channels. With potentially such large sums involved, remittance service providers, policy makers and regulators are always very keen to get a better handle on what is happening on the ground.

The Central Bank of Kenya is taking a leading role on remittance data

Kenya is one of only a few countries in Africa that is responding to the demands of industry and publishing its monthly remittance data broken down by corridor through the Central Bank of Kenya. The CBK also conducted a Diaspora Survey in 2021 and is underway with a household remittances survey in conjunction with the Kenya National Bureau of Statistics (KNBS) and FSD Kenya.

Surveys are incredibly important to support the quantitative data and qualify and provide more insight into behaviours, trends, barriers, and opportunities. However, surveys are not always best placed to identify and accurately quantify the value sent through informal channels. First, people are not always happy to share in a survey-setting that they are using informal channels and secondly, they are not always aware that the channels they are using are informal.

Unique insights from one-on-one interviews

In 2022, FSD Kenya commissioned DMA Global, a development consultancy specialising in diaspora-related affairs and remittances, to explore the use of informal channels for remittances and low-value trade payments sent by MSMEs between Kenya and Tanzania (back-and-forth) and Kenya and Uganda (back-and-forth).

A chain-referral sampling method (snowball sampling) was used ensuring that different segments of society, geographies and purpose of transfer were represented. The research conducted one-on-one interviews with 103 senders across the four corridors, 23 MSME business owners and 13 informal service providers.

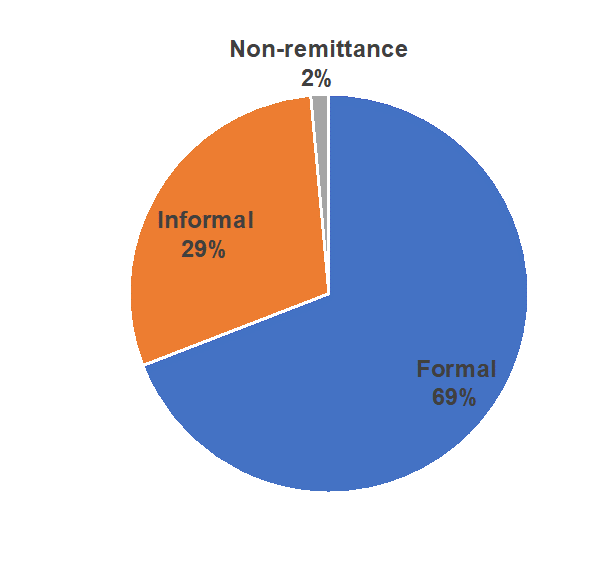

Most people are using formal channels

The main finding from the research was that the preferred method of nearly 70% of senders was through formal channels. The most popular channel for the majority was services offered by the mobile money operators in the market (e.g. sending money from Safaricom M-PESA to MTN in Uganda).

Other popular choices included digital money transfer operators, (including services offered by Western Union, WorldRemit and ChipperCash) and the banks (Equity, KCB etc), especially for larger values.

Preferred Remittance channel for participants sending and/or receiving remittances across four corridors in the East African Community, n=68

Fluidity of people and payments using multiple SIMs

Another key finding was that for many remittance senders and business owners sending money cross-border in the region, their payment methods were as hard to keep up with as their movements.

There were several people interviewed who travel regularly between their country of origin and their country of business or residence. Given the ubiquity of mobile money across the region, this group have multiple SIM cards (and multiple mobile wallets) and maintain a float in each wallet to cover expected costs.

They use a variety of methods to achieve this: topping up their mobile wallets at the border; changing cash as they travel; cross-border bank to bank transfer; and cross-border mobile-to-mobile money transfer. They then initiate domestic payments from their respective mobile wallet depending on the country where the payment is needed. This behaviour, from an accounting perspective, makes it challenging to detangle and identify exactly where the remittance or cross-border transaction is taking place and the method being used.

Digital informality

With a new understanding of the way mobile money is being used, the team saw another widespread pattern of behaviour within these four corridors, namely the practice of informal channels using digital means.

This method sees a customer going to an unregistered / unlicenced mobile money “agent” who provide a cross-border money transfer service for them. As an example, in Uganda, M-PESA is not licenced as a mobile money operator and is not permitted to have mobile money agents in the country. However, there is demand from people living in Uganda to send money to M-PESA accounts (in Kenya) or to top up their own accounts. As such it is possible to find M-PESA “agents” active in Uganda that allow people to either top-up their M-PESA wallet or will send money on your behalf to your family or friends M-PESA wallet in Kenya. The unregistered M-PESA agent accepts Ugandan Shillings from the customer and tops up their wallet in Kenyan Shillings or sends Kenyan Shillings on their behalf. For many senders using this method they did not know that their preferred method is informal, given that the “agent” was using formal, well-known brands. The practice is not unlike the traditional understanding of the Hawala system, but with an updated digital approach.

The research also showed the prevalence of people in Kenya sending money to roaming M-PESA wallets in Uganda to then be cashed out with an unregistered M-PESA agent in Uganda. It should be noted that this was not unique to M-PESA and there were cases of people using unregistered MTN agents in Kenya too. This is something that M-PESA has made efforts to address when a few years ago it deactivated the roaming facility from agents’ handsets. This research suggests that the practice is still alive and well, with ‘agents’ finding ways to circumvent this restriction, perhaps using personal accounts.

Informal services meeting the needs of customers

Understanding informal channels and why people use them shows us that the formal methods available are not wholly meeting the needs of its customers. Most of the people interviewed were formally financially included and did not have barriers to accessing formal services.

Again, for the most part, people were not choosing informal providers to avoid Anti-Money Laundering/Counter-Terrorism Financing restrictions or for tax evasion or to conceal illicit flow of funds. The reason that people were opting to use these informal agents was, for the most part, that the service they are providing is convenient, trusted, and affordable.

For many they were also unaware that the service they were using was not a formal service. If someone is offering the services of a formal provider (M-PESA/MTN) with the logos, then the customer sees no need to question it. For others who did know that the “agent” was using informal practices (a minority of participants), they were not too concerned and considered their agent to be cheaper than the formal cross-border services being offered by the mobile money operators.

So, what can we learn from this?

Customers enjoy the convenience of being able to send money cross-border using their mobile wallet and want to be able to top-up their wallets from any country in the region. There is a clear demand for better interoperability between banks and mobile wallets across the region. With free movement of goods and people within the East Africa Community comes people wanting free movement of their money too.

This study reiterated the need for formal services to be as convenient and price competitive as informal providers in order to compete and shows there is an opportunity to improve the awareness of formal mobile cross-border services. For this there needs to be better transparency around which operators are offering which services in the market and their respective pricing (fee and forex margin) and pay-out options. This requires an easy way for people to be able to compare the pricing of operators and different service providers upfront – before making the payment – and to have confidence that their providers will maintain their competitive pricing over time.