BY:

Advancing inclusive finance: Understanding youth exclusion through a gender lens - Insights from the 2024 FinAccess Household Survey

March 19th, 2025

As Kenya continues to work towards deeper, quality and impactful financial inclusion, it’s crucial to understand the unique barriers and opportunities that exist for young people, particularly young men and women. The 2024 FinAccess Household Survey offers key insights into the financial landscape, shedding light on the challenges faced by the youth and highlighting the disparities between men and women.

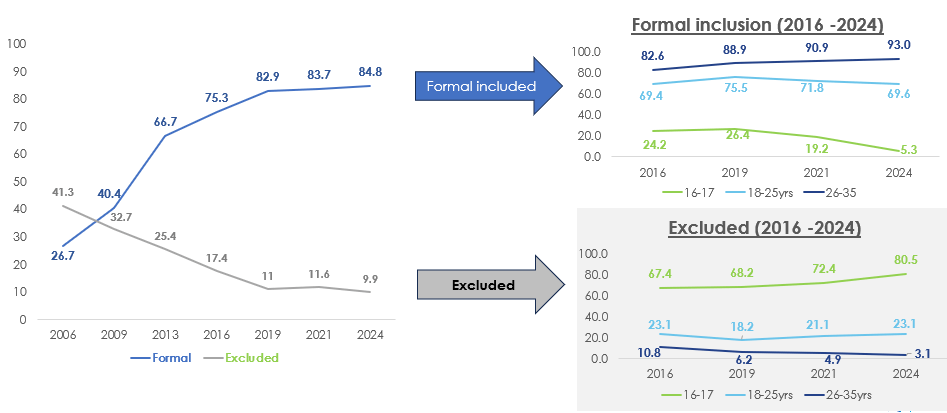

While formal financial inclusion has plateaued for the general population, there is notable growth in the 26-35 age group. However, the younger 18-25 age group has shown slower growth in formal financial access. Additionally, the 16-17 age group faces significant barriers, particularly around documentation requirements due to the legal requirement of age, which hinder their ability to access formal financial services (figure 1)

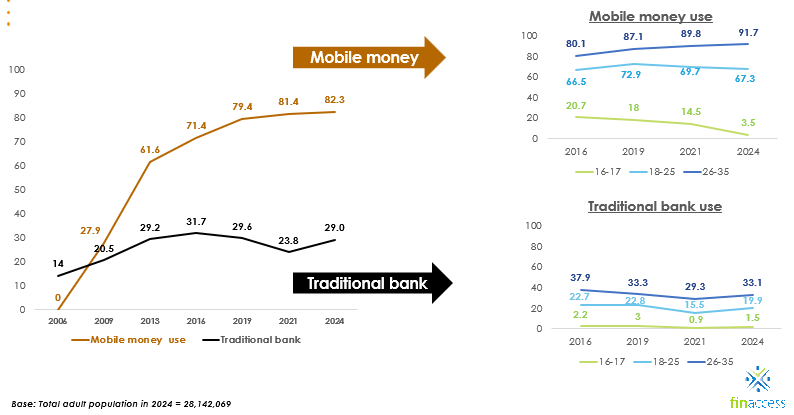

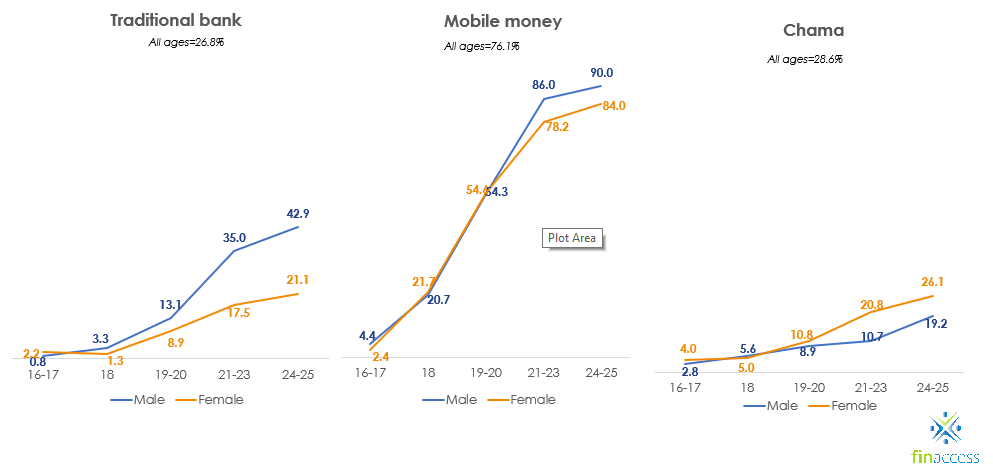

For many young people, mobile money has emerged as a key driver for financial inclusion, and a preferred financial solution, outpacing traditional bank account ownership. This trend is especially evident in the 18-25 age group, where mobile money usage significantly outstrips banking (figure 2).

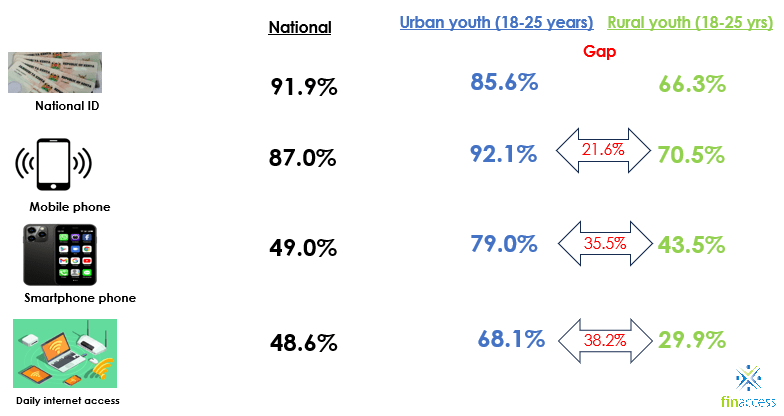

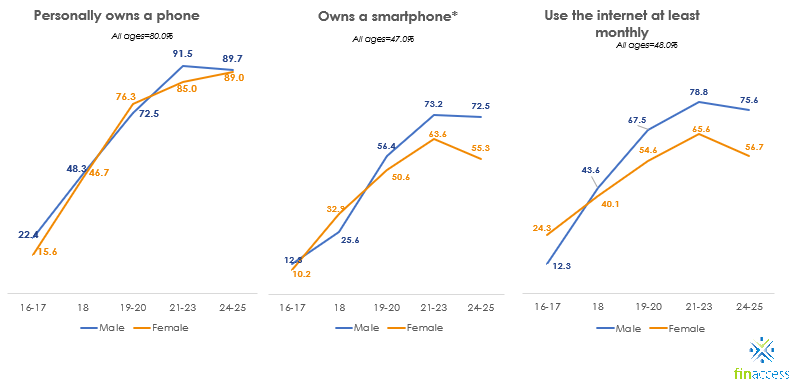

Urban youth are leading the way in digital finance usage, benefiting from higher access to smartphones and daily internet usage. In contrast, rural youth remain at a disadvantage, struggling with lower access to digital infrastructure (figure 3).

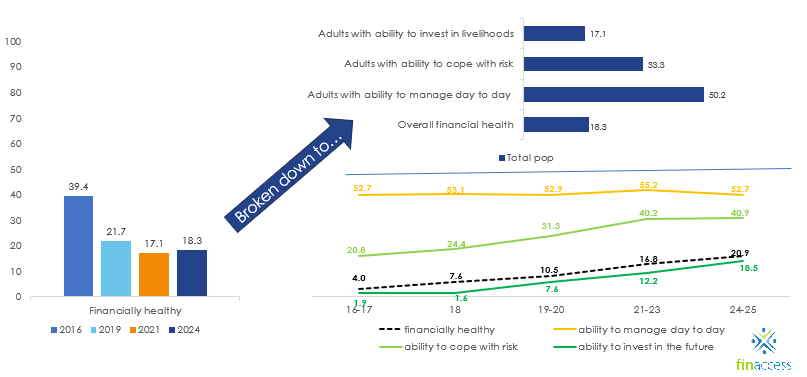

Despite increased access to formal accounts, many young people’s financial health remains low, with income stability and financial resilience still major challenges (figure 4).

The situation is particularly difficult for young women, who face additional barriers in connectivity (figure 5), education (figure 6) and access to economic opportunities, which further limits their financial inclusion.

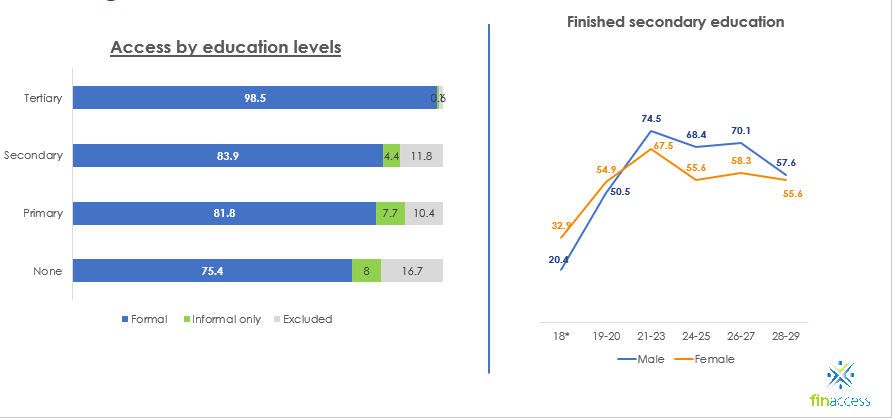

Education levels also influence financial inclusion, with slightly more young men completing secondary education compared to their female counterparts (figure 6)

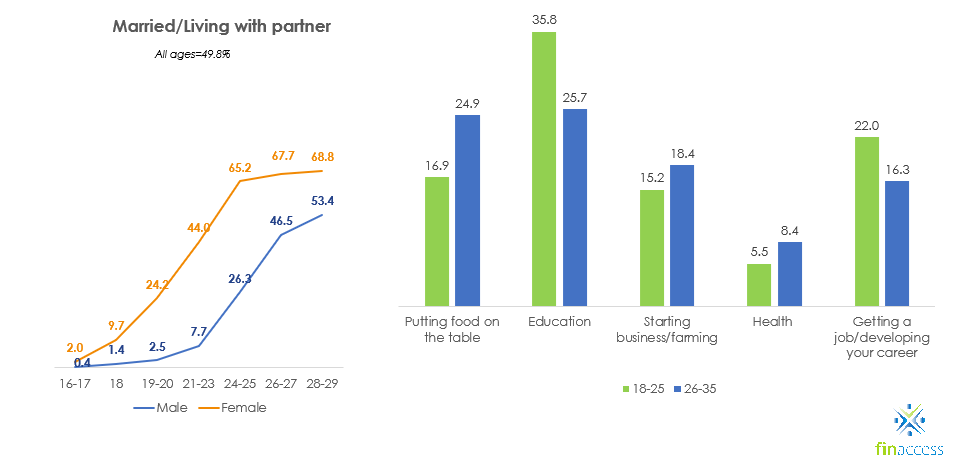

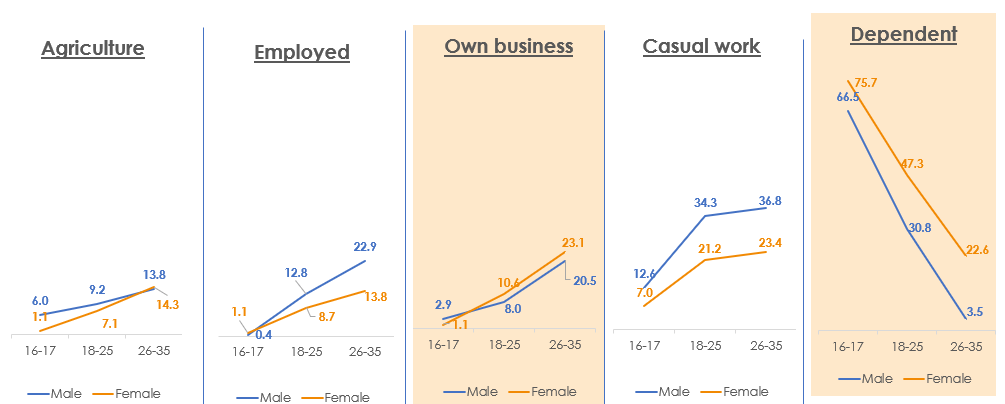

Moreover, marriage and care work disproportionately impact young women’s participation in the economy, often pushing them toward informal labour markets. About half of the young women are married by age 25 hence they are likely taking care of their families (figure 7). Their main life priorities are education and looking for a job.

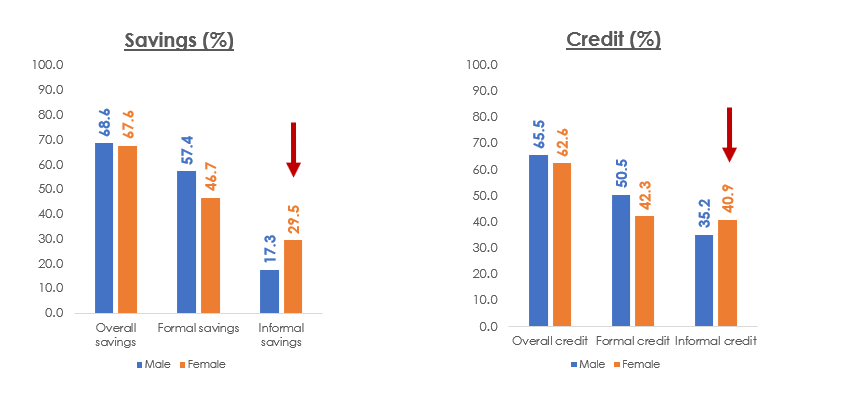

While digital is hoped to bridge the inclusive gap, it is getting wider as the youth get older.. Young women are more likely to rely on informal financial solutions and social networks for savings and credit (figure 7).

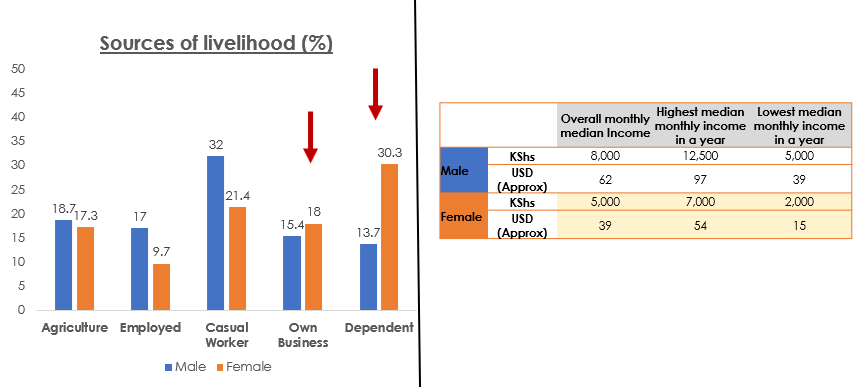

Young women in Kenya have lower participation rates in formal employment compared to their male counterparts. Instead, they are more reliant on casual labour and Micro and Small Enterprises (MSEs). This is most likely because they offer more flexibility to align with their home responsibilities.

Even when the young girls get older, majority are dependents participating in care work. Their income levels are also lower than men, reflecting the informal nature of much of their work – they mostly rely on casual labour and running their businesses. (figure 10)

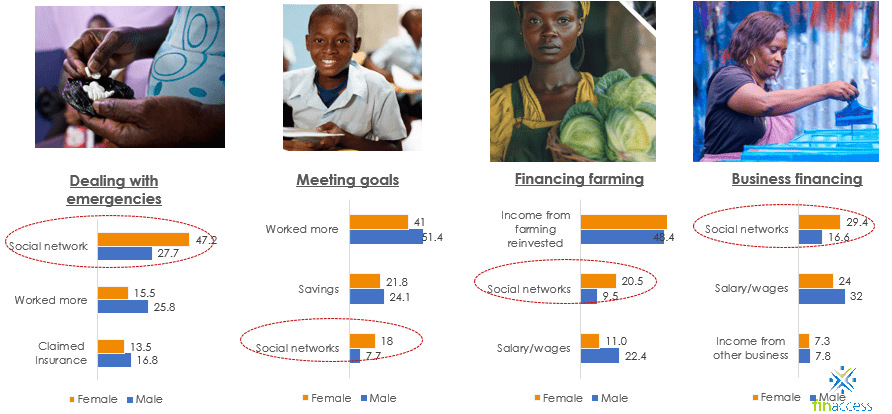

The formal and informal divide persists, with women continuing to rely on social networks for savings and credit (figure 11). These networks are clearly valuable assets, and financial service providers should begin to recognise and incorporate them, as they should be – social assets – when designing solutions.

Looking at the top 3 solutions that women use to finance their needs, informal use of solutions dominates in supporting women to meet their financial needs.

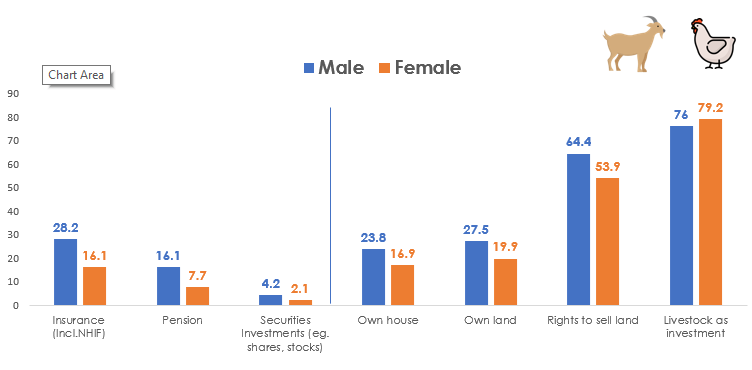

Men dominate long-term investments such as insurance, pensions, securities, land, and housing, except for livestock where women have a stronger presence (owning mainly shoats -sheep/ goats – and chickens) (Figure 13) If social networks were recognised as valuable financial assets, much like these traditional investments, how might this shift women’s participation in the formal financial sector?

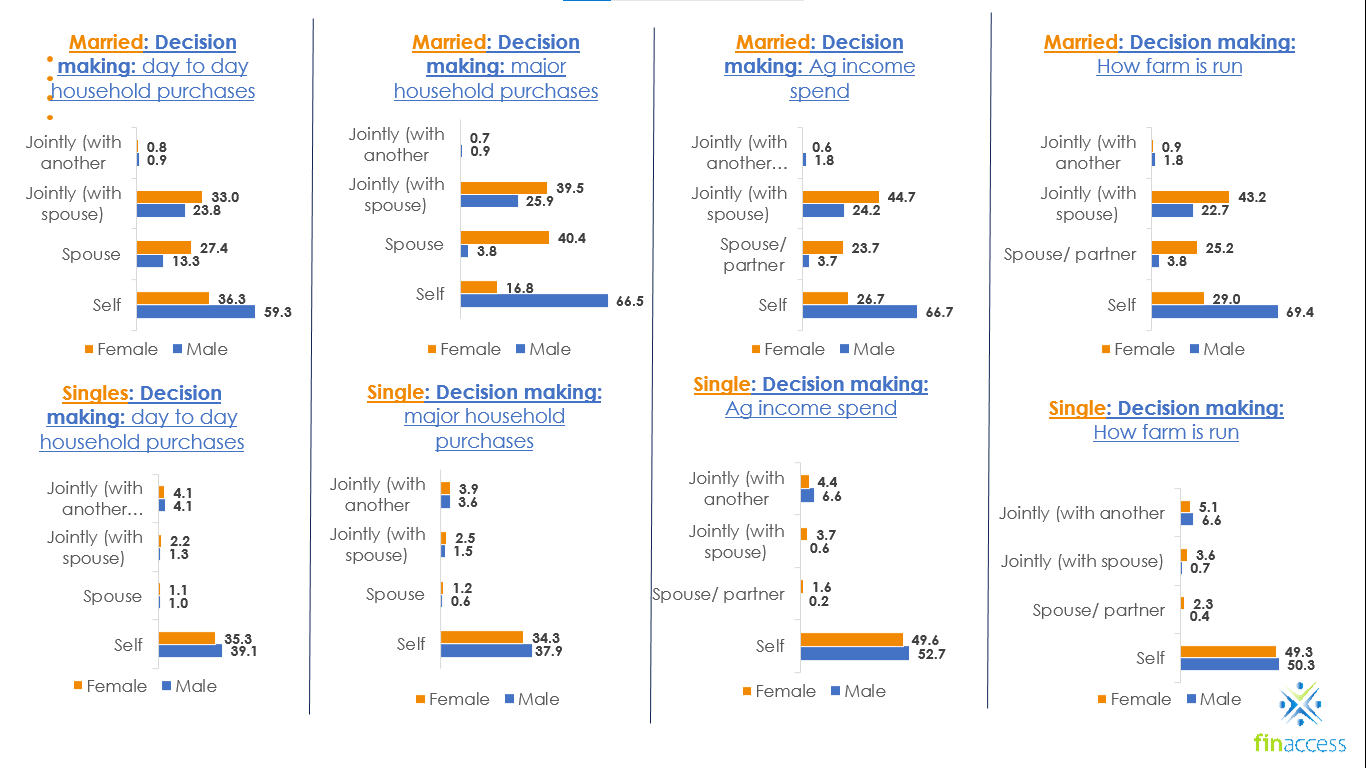

Just as limited ownership of traditional investments hinders meaningful participation in the financial system, the male dominance in household financial decision-making further restricts women’s control over savings and spending (Figure 14) This gender disparity directly affects women’s financial autonomy and long-term economic stability, reinforcing existing barriers to their full inclusion in the formal financial sector.

Conclusion

While digital finance plays a crucial role in improving financial inclusion for Kenya’s youth, it is not a silver bullet. It must be supported by efforts to stabilise income and enhance financial resilience. Rural youth, especially young women, face significant barriers to accessing formal finance, which could be addressed through inclusive and gender-sensitive policies and solution design

Industry players, alongside policymakers, must continue innovating and designing solutions that are inclusive of all youth, bridging the gender and digital divides to create a more equitable financial future for Kenya.

These insights from the 2024 FinAccess Household Survey emphasise the need for targeted strategies to overcome these challenges, focusing on the unique needs of both young men and women in Kenya’s evolving financial landscape, even as they get older.