BY:

The status of MSE finance in Kenya: An update with demand-side data

May 28th, 2024

The Government of Kenya’s emphasis of the ‘hustler economy’ has focused attention on micro and small enterprises (MSEs) as a building block for ‘bottom up’ growth. This is resonating across the financial sector, with providers like banks and SACCOs paying more attention to MSE markets. Digitisation is also opening up access to finance for MSEs. Despite advances in MSE financing, however, MSEs face growing challenges and declining opportunities. Recent data from the FinAccess MSE Tracker survey reveals the latest trends in MSE financing.[1]

Digitisation and payments

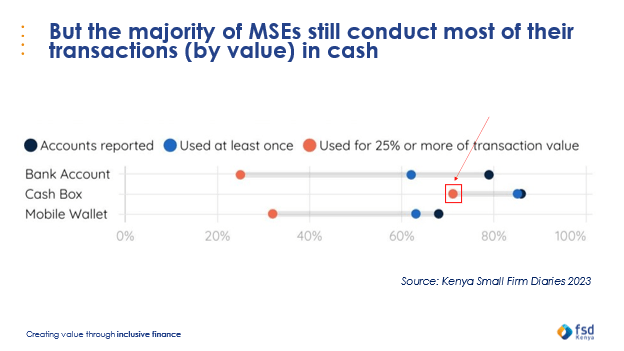

Uptake of digital finance for business transactions has grown exponentially. Alongside this, businesses are becoming more formalised, increasing their visibility to financiers and other market actors. However, the Kenya Small Firm Diaries reveals that majority of transactions by value are still cash-based, indicating that there is still far to go if digitisation is to be a game changer for the majority of MSEs. Qualitative research finds that barriers to digitisation include cost and price transparency; increased exposure and cost of compliance; lack of open data protocols; and systems to support customer ownership and control over data.

Access to finance

Use of digital payments has reduced information asymmetries, opening up access to traditional bank finance and larger ticket longer-term loans and savings. However, bank finance is still more available to men and more organised firms with employees (dubbed ‘small firms’ from the Kenya Small Firm Diaries); women and micro firms still rely on informal finance including chamas (groups), begging the question of why banks are not designing for these segments. Meanwhile, the government’s Hustler Fund, launched in October 2022 has rapidly become the most widely used source of credit for MSEs. However, MSEs who have borrowed from the Hustler Fund state that they mainly use Hustler Fund loans for household rather than business purposes. Nearly half (48%) of Hustler Fund borrowers stated that they had defaulted on their loans, and overall debt stress (reported loan defaults) rose substantially between October 2022 and June 2023.

Working capital

The Kenya Small Firm Diaries finds that businesses mainly need finance for working capital rather than investment. Businesses state that key sources of finance for liquidity are savings and social networks, with 30% also stating that they cross finance their businesses through other sources of income such as farming. Both the Small Firm Diaries and the FinAccess MSE Tracker surveys find that supply-chain finance (goods on credit from suppliers and goods on credit given to customers) is widely used to support business operations. Leveraging Kenya’s existing financial infrastructure (e.g. moveable collateral registries, credit bureaus, digital transaction and business data, warehouse receipts etc.) to reduce information asymmetries and risk would also open up opportunities for finance, including supply-chain finance.

Challenges facing MSEs

Despite the considerable advances in MSE financing, the underlying picture for MSEs is bleak. Increasing pressure from macro-economic and global shocks including inflation and Covid-19, result in increased cost of supplies and weakened demand which dampens revenues and profits for MSEs; while increased pressures relating to compliance and fees combined with weak market infrastructure further compromise MSE resilience.

This strain is evident in the decreasing proportion of the adult population able to earn an income from business since 2016; and a 20% decrease in MSE incomes during the Covid-19 period (FinAccess 2021).

Better financing is only one piece of the puzzle to set MSEs on a stronger pathway, and enable them to fulfil their role in driving inclusive growth. In addition to leveraging existing financial infrastructure and innovating to develop more tailored financial solutions, MSEs need proactive policies to strengthen demand (for instance through universal social protection): reduce cost of supplies (e.g. investment in local value chains and supply-chains); strengthen market infrastructure and streamline the cost of compliance to align more closely with business revenue and firm financial health.

Finally, research and information play a significant role in supporting policy and business development for MSE financing. In this regard, the government’s investment in FinAccess MSE Tracker surveys is laudable. Added to this, if the government were to finance a long-overdue update of the 2016 KNBS MSME survey, this would be a significant boon for Kenya’s hustler economy.

This blog is one of the articles in FSD Kenya’s 2023 annual report. To read the full report, click here.

[1] This analysis is based on comparisons with FinAccess Household survey data and FinAccess MSE tracker data. The FinAccess Household surveys are nationally representative of individuals aged 16+ in Kenya, and include a sub-sample of those who state that they earn income from business (MSEs). The tracker surveys are further sampled from the FinAccess household survey MSE segment, who are still in business at the time of the tracker, and are willing and available to be reinterviewed. These surveys are therefore not strictly comparable, but they are indicative of trends and developments in MSE financing as we await FinAccess 2024.